To every beginning, there is an end. An Alpha and a…. $THETA?

This fundamental analysis is a sneak preview of an up and coming premium newsletter from Crypto Consulting Institute. For more information visit: https://www.cryptoconsultinginstitute.com/newsletter

From a fundamental perspective, the likes of Theta is a pleasure to cover.

Why?

Because most cryptocurrencies are only considered a means of value transfer, the utility of the underlying technology is often overlooked.

With this in mind, it is not premature to state that Theta is a contender in the quest for utility with a value proposition that is not impossible for the average investor to wrap their head around.

It is no politically slanted hypothesis that centralized content delivery and social media platforms are increasingly endorsing censorship. Content creators need greater control over their content and fewer barriers to establishing a platform. Putting aside the politics of censorship, the high costs associated with content delivery are not widely appreciated.

Typically, the likes of YouTube would be responsible for powering and maintaining servers to ensure viewers can stream content available on the platform. These are significant overheads that increasingly prompt the platform to rely on advertising to cover the content delivery costs. Counterintuitively this also impacts content creators. More views lead to higher prices for data storage and delivery. These demands impose the need for content creators also to endorse advertising. Not only to make a living but cover the costs of having their content stored and delivered. From the audience’s perspective, this impacts the quality of viewing when you’re suddenly interrupted multiple times with targeted advertisements.

Theta is a cutting-edge solution, not only to give content creators total freedom but to enable a method of content delivery that will significantly reduce associated costs.

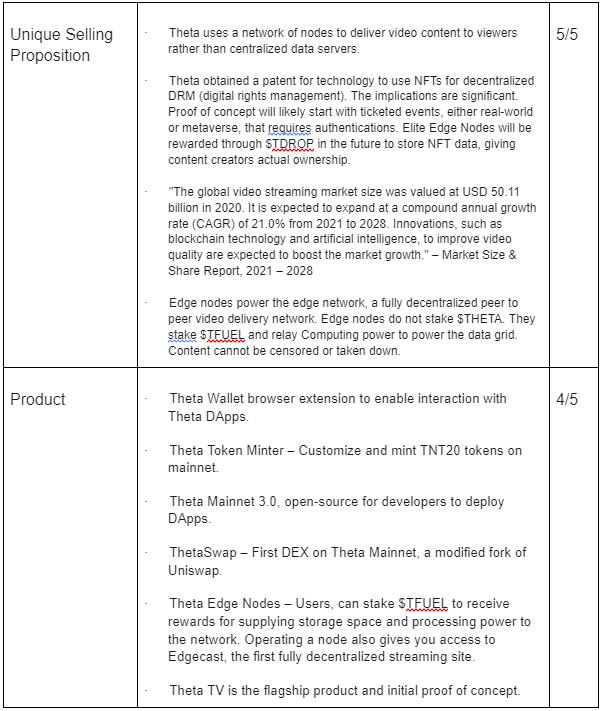

Their value proposition is a cut above the rest in terms of having DApps1 that can stream permissionless content and laying out the infrastructure that can meet the needs of many different DApps. The developments made so far indicate the team are proficient and know what they are doing. The 130,000+ active edge nodes on the network along with their large followings on their socials speaks volumes as to the popularity of the project. For this reason, we will explore the implications of this technology going into the future, what black swans may inhibit adoption, and what you’re all eagerly waiting for — price predictions from the current bull market as we progress into the future.

Theta Key Summary;

Web 3.0. is coming.

There is no clear-cut definition of Web 3.0 as innovative infrastructure continues to emerge. At this point, it refers to a technological undertaking that envisions a complete overhaul of the internet as we know it.

Web 1.0 was the first stage of development for the internet that primarily consisted of static websites and archiving — a global library.

Web 2.0 that we are using right this moment builds upon user-generated content and applications.

Web 3.0. is ambitious in the integration of AI processes into smart devices and blockchain technology. Two-thirds of all data consumption is attributed to live-streaming videos. This trend towards users being hungry for video content has placed a tremendous burden on content delivery platforms to upgrade and maintain their storage and delivery infrastructure.

Theta’s flagship product is Theta TV (https://theta.tv), a decentralized streaming service that does not deliver content from a single data repository. Instead, 130,000+ Edge Nodes lend their processing power and storage space to store fragments that are collated upon delivery to the end-user.

This concept is not new for those with experience downloading movies, music, and TV shows online through torrents that operate on a peer-to-peer (P2P) basis, whereby you download a file from hundreds of users rather than from a single source. Why this model has not been meaningfully expanded upon by existing streaming services is from the lack of incentives for uploaders to maintain the network.

The capabilities of Theta’s infrastructure go beyond decentralized data storage for content delivery. With the recent release of Theta Mainnet 3.0, Theta can start asserting its presence as a decentralized data storage solution for non-video content across different blockchains.

Furthermore, Theta is explicitly seeking to expand into NFTs. Purchasing an NFT from Theta’s NFT marketplace allows you to acquire an NFT and a role in storing your portion of it through giving idle bandwidth and storage capacity to the Theta Network. What this enables are NFTs to take on a format beyond a 2D or 3D image. A decentralized data storage solution could store more resource-intensive forms such as music, videos and gaming NFTs.

It appears that future developments are looking to utilize NFT storage and content delivery capacity to live streams inside Metaverses. Theta was recently awarded a patent for its use of NFTs in digital rights management. The implications of having intellectual ownership over their NFT storage and content delivery method cannot be understated. Theta, among many other competitors, is currently experimenting with NFTs for ticketed events, a clever starting point for proof of concept. Insofar as NFTs are immutable with a fixed supply that cannot be forged. There is clear value in utilizing the technology to authenticate guests attending digital and real-world events.

Theta Labs team have a wealth of experience in building Web 2.0. Steven Chen as a co-founder of YouTube, understands the limitations of the existing methods of content delivery. Primarily that existing infrastructure needs to be improved to accommodate the exponential growth of mobile and internet adoption.

Different shades of Theta

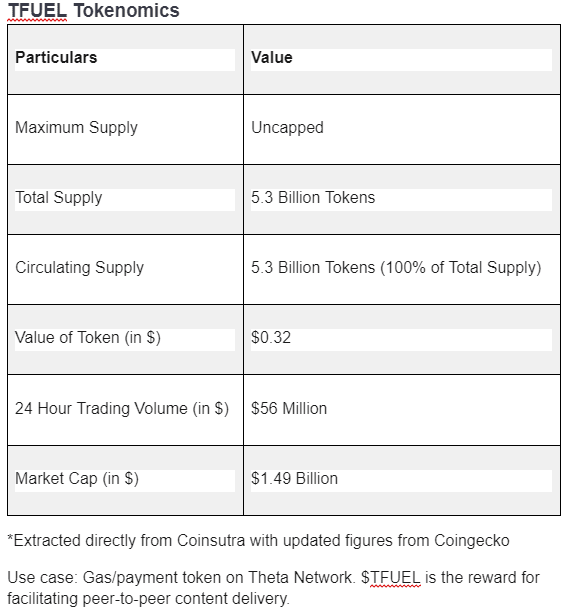

*Extracted from Theta Ecosystem 2022 and TDROP Whitepaper.

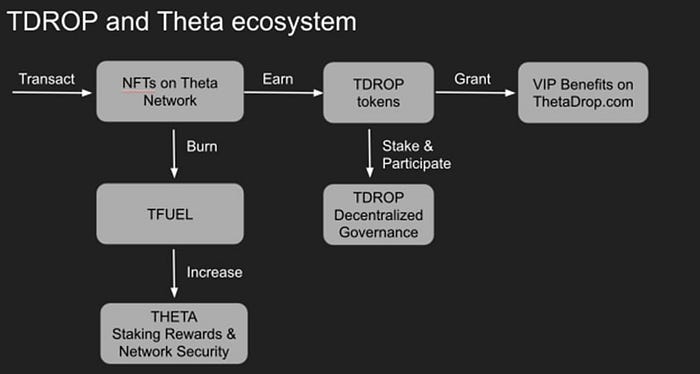

*Extracted from Theta Ecosystem 2022 and TDROP Whitepaper.

Use case: February 1st 2022, is a tentative date for $TDROP to go live. This token will incentivize users to purchase NFTs with $TFUEL and receive $TDROP rewards. Edge Node participants will also receive a share of 1% of all gross sales through NFT marketplaces on Theta.

The Fall Is High From Up in the [Data] Cloud. — Discussion

Theta is one of the most straightforward value propositions to emerge in the cryptocurrency space that does not leverage the ‘storage [or transfer] of value’ narrative. It requires little explanation as to the value this infrastructure will bring. However, Theta’s mission to become the Magellanic cloud of the digital universe is not a given as the path is fraught with challenges.

If you have read previous FAs published in the CCI Newsletter, you will be comfortable with the notion that decentralization exists on a spectrum. Too much decentralization, and the egg cannot be unscrambled or modified. Too much centralization leads to excess oversight and interference. A common starting point is to have a highly centralized operation that transitions further and further toward decentralization as the project ecosystem further develops.

However, there is a balancing act for Theta Labs to weigh up the interests of everyday investors and big corporations. One of the most bullish aspects of Theta is the big-name partners like Samsung, Sony and Google cloud that participate in validating the network. However, the limited involvement of other entities to keep these big players in check is a valid concern. While the edge nodes are decentralized, the base validation layer is undeniably at the whim of centralized entities with separate, and perhaps sometimes opposing, interests from individual investors and users. Though by and large, $THETA token holders benefit from the involvement of prominent corporations.

Those with an in-depth understanding of blockchain technology value decentralization to ensure power resides in the hands of the people. All technology is agnostic, but the users or primary stakeholders are most certainly not. Microwave energy can cook food or create weapons of inconceivable destruction. Many that have spent time in cryptocurrencies may invariably base their investment decisions on decentralization. The continued dominance of TVL on Ethereum despite the insane gas fees is a good indication of this to be the case.

While the many tokens of Theta incentivize different levels of user activity and participation, the problem with having additional tokens is fragmented liquidity. New tokens do not automatically lead to new liquidity entering the ecosystem. Instead, investors will likely sell some of the existing tokens for the new one. $THETA and $TFUEL appear not to share this correlation when they began their upward march in December last year. Since then, $THETA has not held up in price as well as $TFUEL.

There are plenty of cautionary tales to consider with introducing the $TDROP token as to how fragmented liquidity manifests. The rising activity on the Binance Smart Chain and the Pancakeswap copy/paste jobs riddled the ecosystem is a clear example of fragmented liquidity. Many who chased high APR2 returns soon realized that the gains diminishing compared to when there were fewer options in the beginning. Shortly after that, many of these newer protocol tokens were seen to have prices obliterated.

Why?

There was no reason to hold these tokens without a clear use case. However, tokens in the Theta network do have utility. Those who value freedom of speech and recognize the value of decentralized data storage for content delivery will flock to this. While people often invest and utilize technology according to their values, they also don’t fancy investing in an incomplete product. Theta has made significant developments and does have a working product. Still, it does not currently rival the likes of YouTube in terms of volume, diversity and quality of content available. If censorship continues to intensify in the macro, we can expect that the likes of Theta will attract more content creators.

As far as competitors go, no one comes close to offering fit-for-purpose infrastructure like Theta. However, this does not mean they have a monopoly on the value proposition. Livepeer and Verasity are two projects with solid value propositions with different approaches to enabling decentralized video streaming platforms. The former leverages the most decentralized virtual machine there is, Ethereum, to build a content delivery protocol. The latter has produced a patented protocol that utilizes Proof of View (PoV) consensus to secure and deliver video content. These competitors do not have the backing of major tech companies that are actively looking to integrate Thetas blockchain technology to reduce costs and increase the resilience of their networks.

While Theta’s infrastructure is a cut above the rest for content storage and delivery, a hidden category of cryptocurrencies poses the greatest threat to their market dominance. The likes of Aleph, Filecoin, Siacoin and Ocean could very well play a role in facilitating infrastructure for projects such as Verasity and Livepeer. Interoperable layer-1 blockchains such as Kardiachain, Polkadot and Cosmos may link Dapps cross-chain with the necessary infrastructure. For this reason, decentralized data storage, interoperability and transcoding content to be delivered are a primary focus for Theta. While it appears they may be competing on one front of content delivery where they seem to dominate, they are, in actuality, competing against interoperable and decentralized data storage projects.

So, where does that leave us on Theta as an investment opportunity?

We can expect the price to maintain some degree of resilience in the short term, given that 60% of $THETA is locked up for stakers to be eligible for $TDROP airdrops until February.

While nothing is outside the realm of possibility in a bull market, it is unlikely that Theta will realize a parabolic bull-market climb to realize true market value until their infrastructure reaches full maturity. Adoption is still very much ongoing. Confounding variables in this hypothesis would be the onboarding of new partners. Also, whether Theta Mainnet and hack-a-thons attract new development will determine Theta’s short-term price action.

Mid-term price action will be dependent on how big investors and partners utilize the technology. Suppose Sony decided to activate every Playstation console and television in their network to power Edge Nodes. If decentralized data storage solutions facilitated Samsung’s services and Google Cloud Storage, we could expect significant hype to drive the price of Theta.

Theta is a long-term investment. It is one of the few cryptocurrencies we can reasonably hypothesize will still exist in three years for the next bull market, assuming the market continues to respect Bitcoin’s halving cycles. Continued demand for video streaming services will require content providers to seek methods to reduce costs and increase efficiency. Theta will likely be needed to meet this rising demand. As content regulation continues, we can expect content creators to migrate their content over to the likes of Theta, accompanied by their subscriber base.

There are comparable projects to understand how $THETA has yet to realize fair market value. Singularity Net ($AGIX) is building AI Machine learning on the blockchain. But, until smart devices become common in households or robots deliver your mail, it is unlikely they will realize parabolic price increases until the demand is there. Energy Web Token ($EWT) is another example that will incentivize users to monitor their electricity usage and utilize renewable sources in exchange for rewards. Again, the adoption of smart appliances is lagging behind developments in the back end and integrating applications onto the electrical grid is not a small undertaking.

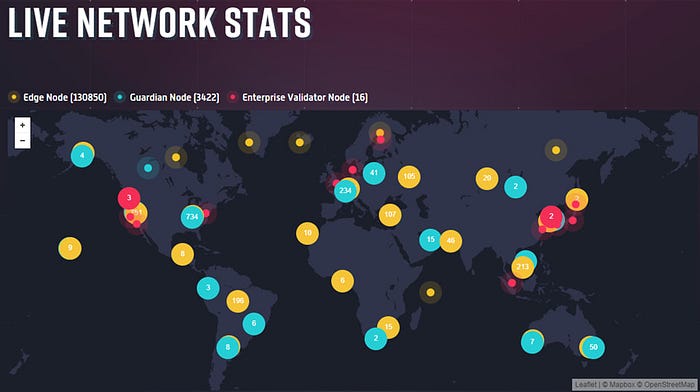

While Theta’s previous all-time high may not escape the rearview mirror during this market cycle, it is simple to accept the proposition that Theta at a $6.3B market cap has room to grow. If 99% of all crypto projects were to fade from relevance, Theta may stand the test of time to be among the 1% that survive.

References

Cisco Annual Internet Report 2018–2023: https://www.cisco.com/c/en/us/solutions/collateral/executive-perspectives/annual-internet-report/white-paper-c11-741490.html

Medium: Theta https://thetalabs.medium.com/

Medium: Theta Labs awarded US Patent 11,153,358 for “Methods and Systems for Data Caching and Delivery over a Decentralized Edge Network” https://medium.com/theta-network/theta-labs-awarded-u-s-dd3a3340f0d6

Theta Website: https://www.thetatoken.org/

Theta Whitepaper: https://s3.us-east-2.amazonaws.com/assets.thetatoken.org/Theta-white-paper-latest.pdf

The $TFUEL Use Case: https://medium.com/theta-network/the-tfuel-use-case-ea666d042aa2

Theta Network analysis: https://coinsutra.com/theta-network-analysis/

Theta Network — An Essential Infrastructure for Metaverse Development: https://medium.com/theta-network/theta-network-an-essential-infrastructure-for-metaverse-development-2cf78f1c1e04

Theta NFT Marketplace — https://www.thetadrop.com/

Youtube, THETA & TFUEL: Could They Break New Highs??

Youtube, THETA TOKEN IS A LONG-TERM PLAY! (NASA, TREZOR FIX, NEW PATENT) CAN IT REACH $35 BILLION IN Q4?

Video Streaming Market Size, Share & Trends Analysis Report By Streaming Type, By Solution, By Platform, By Service, By Revenue Model, By Deployment Type, By User, By Region, And Segment Forecasts, 2021–2028 https://www.grandviewresearch.com/industry-analysis/video-streaming-market